“We are 12 years in NDC and very low adoption”. Kurt Ekert, Sabre CEO, talks about NDC, Offers and Orders, after publishing the 1Q 2024 company results. I’ve listened to his interview with Linda Fox and read the results… between the lines

Disclaimer: I’m just an observer of travel technology, not a financial analyst

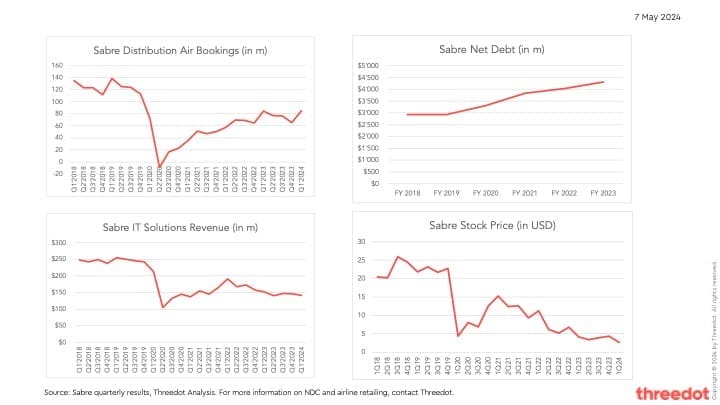

First I’ve looked at two key business indicators: air bookings and revenue from IT solutions

- Air bookings: Sabre processed around 130m air bookings per quarter pre-Covid. It has reached 85m in 1Q2024 compared to 84m in 1Q2023. Will it recover to pre-Covid figures? Where have the 50m missing air bookings gone? What is 1m growth in one year compared to industry’s 5% growth? Should reported air bookings be split between EDIFACT and NDC? How will NDC air bookings translate into revenue in the future?

- IT solutions: Sabre had about $250m of revenue per quarter from IT solutions per-Covid. It was $141m in 1Q2024, down from $152m in 1Q2023. What are the plans for new IT solutions supporting offers and orders? What are the recent announcements, similar to Amadeus with Nevio or Farelogix / Accelya with their NDC API?

Then I’ve looked at two key financial indicators: net debt and free cash flow

- Net debt: Sabre had about $3b of net debt in 2018. Post-Covid, the 2023 net debt is $4.3b, up from $4b in 2022. Depending on interest rates, the debt represents a significant financial cost. Sabre may have to refinance debt and repay maturities.

- Free Cash Flow (FCF): Sabre has generated $95m of negative FCF in 1Q2024, worse than $90m negative FCF in 1Q2023. FCF can be used to repay the debt or allocated for capex to invest in new technology. A healthy company has enough FCF to repay the debt in a couple of years. When will Sabre generate enough cash to repay the debt and invest in technology? In the meantime, Amadeus reports strong FCF growth, above $1.1b in 2023.

Finally I’ve looked at how investors value the company and its strategy

- Stock price: it was in the $20s before Covid, with a $26 high in 2018, but is now close to the lowest point, at $2.58 on Friday, sending the market cap below $1b. While the air travel industry has largely recovered from Covid, Sabre’s stock is 90% below its high. In the meantime, Amadeus closed at €59.56 on Friday, roughly at the same level as 2018, and only 25% below its high in 2019.

It’s not easy to reconcile these numbers with the latest optimistic announcements. Are the fundamentals really in place to drive future revenue (from air bookings and IT solutions) which can generate enough cash to repay the debt and invest in new solutions? Airlines and travel agents need IT vendors capable of running critical systems at scale.